I keep seeing the “there’s no market for entry APS-C cameras” statement being batted about the Internet.

Last year Japanese digital cameras shipped 8.8m units (compacts plus all ILC). That represented a value of 420b yen. I’ve noted before that the Japanese are trying to keep that overall number as high as possible, because it drives component costs, spread of R&D and manufacturing dollars, overhead, and more.

While one tactic the camera makers are using is trying to get you to transition to higher-priced full frame mirrorless cameras, the other tactic they’re using is to fill their lines with other things that will sell.

In terms of volume, APS-C is the image sensor most of the ILC units currently sold are using. The average selling price of those bodies is under US$1000.

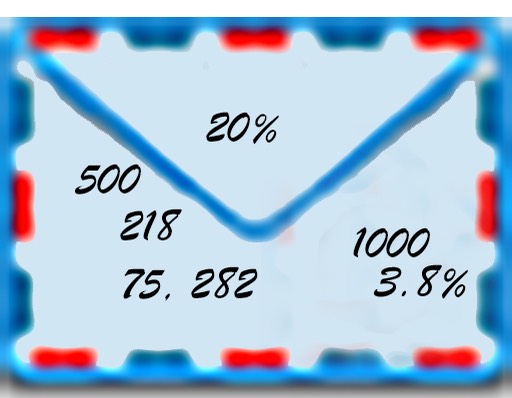

So let’s get out our envelope and pencil some numbers on the back.

Assume 5m units and 500b in revenue (rounded numbers from where we’re currently at). That’s US$1000 a unit, though that’s not the final sale price, it’s what the camera company took in.

Next, we have to make an assumption about APS-C versus full frame. Nikon’s been pretty successful at full frame. They’ve never sold more than 20% of their units as full frame, though. The same appears to be true with all the other makers, as well. So let’s say 20% of those 5m units are full frame, which is a nice round 1m units (warning: I’m pretty sure that number is higher than current full frame volume, but we’re just sketching out some numbers to show you the reason why the statement in the first paragraph will prove wrong).

Let’s further assume that those 1m full frame units sell for an average of US$2000 (warning: also likely too high a number). That’s 218b yen. The camera companies still need another 282b yen of revenue to keep their heads above water. 75b will come from compacts, but we’re actually now short almost equal to the revenue from full frame to make our 500b yen number. That has to come from crop sensor ILC.

What number would make that work? How about 3.8m units at US$500 average? (Again, that’s not the retail price, it’s the price the Japanese sold the unit into distribution for.)

Can the Japanese sell 3.8m APS-C units a year? They already do. And they’ll be highly motivated to make that number work going forward. Not only does it keep the overall dollars taken in at an acceptable level, but it also generates new potential customers to later upgrade to full frame.

Of course the issue is going to be driving as much cost out of such product as possible while providing as much benefit as possible (over a smartphone) at the same time. That’s a tight, tough design space, but when you know what it is you have to achieve, that’s more than half the solution to the problem. If you don’t know what you have to achieve, you will only solve the problem by random chance.

This, by the way, is Canon’s conundrum. The M series was designed to be just that: as much cost removed as possible while providing something beyond a smartphone is capable of. The problem is that M doesn’t eventually lead a user to RF. Moreover, since the M’s have a paucity of lenses that go beyond 70mm equivalent, they don’t really offer optical option advantages over the smartphones. That makes the M’s a hard sell.

A Nikon Z30 wouldn’t have the same “doesn’t lead to full frame” problem, but the paucity of lenses (buzz, buzz) still makes Nikon’s problem similar to Canon’s.

Sony is mostly using older cameras to get entry model prices down (e.g. A6000) rather than have a specific entry model (e.g. an up-to-date A5xxx). The Alphas do lead to full frame, and Sony has a better lens set for APS-C than Canon and Nikon, so Sony will more likely succeed in their goals for APS-C than their main rivals.

Fujifilm is “all in” with APS-C. XF doesn’t really lead to GFX other than the brand name on the front of the camera and the film simulations. Fujifilm’s problem, therefore, is different than Canon/Nikon/Sony: Fujifilm either needs medium format to produce more volume or they need even better high-end APS-C cameras. Probably both.

Personally, I’d have a line that had two low “hook them” cameras, and otherwise mostly concentrate on higher end cameras. The trick is how big can you make the gap between the hooks and the big fish you really want to sell. Make that gap too big and you don’t get much action. Make it too small and you don’t get all the dollars you could have.

Getting back to the first paragraph: "there’s no market for entry APS-C cameras”. No, there has to be a market for APS-C or else we’re going to lose a lot of camera makers. They have high motivation to make a low end work, and they are constantly analyzing that trying to get their product optimized to what they can sell.

Ten years ago I published an article and presented to Japanese executives with my thesis: that smartphones would constantly erode the bottom of the dedicated camera market, while the top of the market would basically be full frame. My prediction was that smartphones would first start gobbling low end 1/2.3” sensor compacts, then larger sensor and higher end compacts, then 1”, and eventually start competing with m4/3 and maybe APS-C. Thus, the space between the smartphones and the top full frame cameras would get smaller and smaller.

I called this the Big Squeeze.

We’re deep into the squeeze. But it doesn’t mean that there’s no market for APS-C, it means that the products you can put into what’s left of the dedicated camera market are more narrowly defined and are under price pressure.